Back when most of us parents were in college or working for the first time when we ran out of money for food, we ate ramen. You remember those days! When today’s teens or young adults run out of money, many of them simply put food on a credit card. We must teach them that when they run out of money, they need to eat ramen.

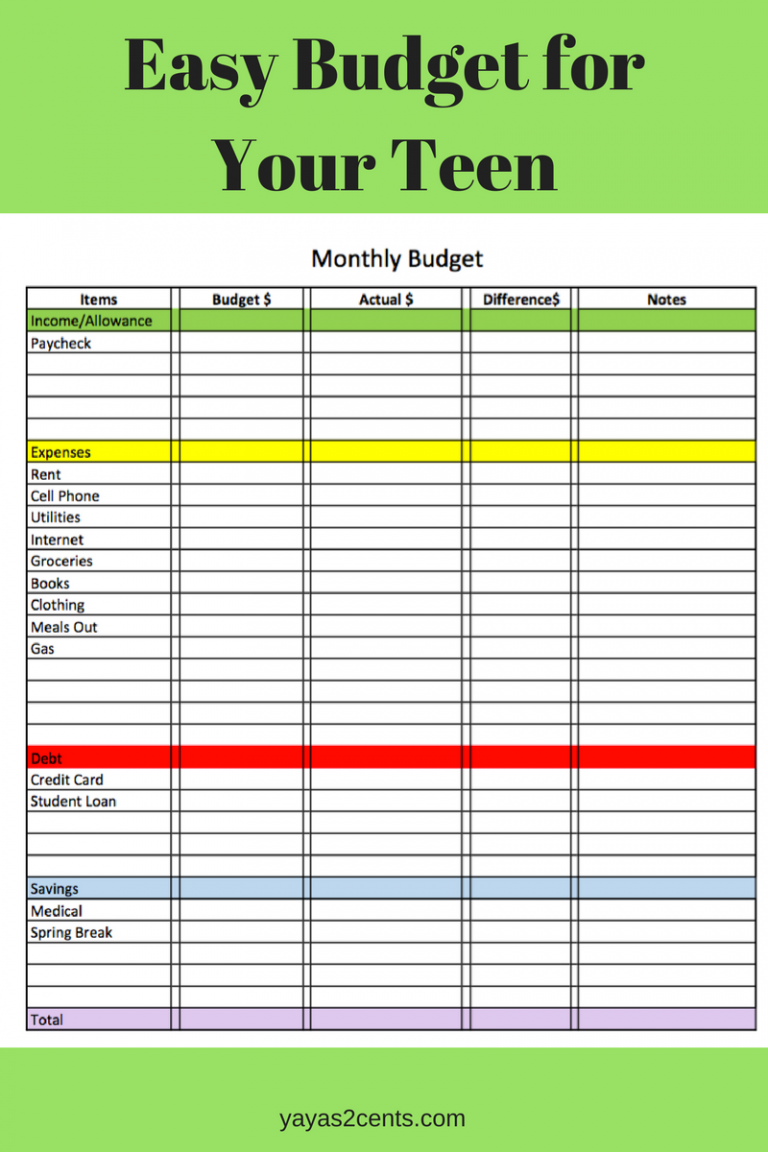

More to the point, help your teens or young adults make a budget. Below you will see a simple budget plans for teens/young adults. They do not have many expenses, so keep it simple. Check out our link https://amzn.to/4r0Rxgt.

Back when most of us parents were in college or working for the first time when we ran out of money for food, we ate ramen. You remember those days! When today’s teens or young adults run out of money, many of them simply put food on a credit card. We must teach them that when they run out of money, they need to eat ramen.

More to the point, help your teens or young adults make a budget. Below is a simple budget plan for teens/young adults. They have few expenses, so keep it simple. Check out my amazon affiliate link for more budget planner ideas https://amzn.to/4bFzwiY